Precedent Transactions

Precedent transactions analysis uses a multiple-based approach to estimate a company’s implied valuation range. It examines past M&A transactions to identify the valuation multiples applied in those deals. This method is typically used to assess the potential sale price range of a company. As with comparable company analysis, selecting the most relevant and comparable past transactions is crucial to ensure the analysis is meaningful and reliable.

This method is mostly used to asses the potential sale range of a company. Like comparable company analysis, the effectiveness of precedent transactions analysis depends on the quality of the selected peer transactions. Identifying deals involving companies with similar business models, size, growth profiles, and market conditions is essential to ensure the analysis is both relevant and credible. As a general rule, transactions that occurred within the past two to three years tend to be the most useful. These deals reflect more comparable market dynamics, industry trends, and investor sentiment.

Under normal market conditions, precedent transactions tend to yield higher valuation multiples than those observed in trading comps. This happens for two main reasons:

- Control Premium: Buyers are typically willing to pay a premium to acquire control of a company. This premium compensates the seller for handing over decision-making authority and full access to the company’s cash flows.

- Scale Economies: Acquirers often anticipate realizing synergies—such as cost savings, revenue enhancements, or scale efficiencies—which justifies paying more than the standalone value of the target.

Below you will find a detailed step by step guide on how to perform precedent transactions analysis as well as a practical example.

1. Identify Previous Deals

Identifying relevant previous deals is the foundation of a relevant analysis. Investors must identify companies with similar characteristics to the target that were involved in recent M&A deals within the last two to three years.

Some of the databases most used to perform precedent transactions analysis are:

- Capital IQ: Offers detailed M&A transaction data, including deal values, multiples, financials of buyers and sellers, and filings.

- Bloomberg Terminal: Offers real-time and historical deal data, including transaction comps for a wide range of sectors.

- FactSet: Offers comprehensive M&A data, particularly strong in U.S. transactions as well as valuation multiples and premiums paid.

It’s important to note that these databases are typically not accessible to most retail investors, as they require expensive subscriptions and are primarily used by professionals in investment banking, private equity, and corporate finance. As a result, conducting a robust precedent transactions analysis is generally not recommended without access to a reliable and comprehensive data source like those listed above.

For this first step, investors are to locate as many potential transactions as they can within the universe previously established. For the initial list, investors should take into account factors as transaction size, geographic location, industry of the transaction and they may take a look at the target’s comparable companies universe.

Other aspects that are relevant when performing this type of analysis include:

- Market Conditions: If an investor cannot find a sufficient number of relevant precedent transactions from recent years and chooses to include older deals, it becomes crucial to carefully consider the market conditions that influenced those past transactions. For example, deals from the early 2000s often featured significantly higher premiums, driven by strong market demand and heightened financial activity during that period.

- Deal Dynamics: Particular circumstances surrounding a transaction.

- Was the transaction paid entirely in cash, or was it a mix of cash, stock, or other securities?

- Was the company sold through a competitive auction process, or was it a privately negotiated sale?

- Was the transaction friendly and supported by the target’s management and board, or was it a hostile takeover?

2. Find the Necessary Financial Information

Locating relevant information for precedent transactions analysis can be challenging for investors. However, information regarding transactions involving public targets is more accessible due to SEC disclosure requirements. For these transactions investors can use EDGAR search for identifying the following:

- 8-K: For public companies is filed within 4 days of the transaction announcement. It contains key details about the deal terms, along with a description of both the target and the acquiring company.

- Proxy Statement: It includes major information about the terms of the transaction, a description of the financial analysis including the fairness opinions of any financial advisor behind the transaction and a copy of the definitive purchase agreement.

- Schedule TO/14D-9: It contains a recommendation from the target’s board of directors to the shareholders on how to react to a tender offer including the already mentioned fairness opinion. The acquirer files a Schedule TO whereas the target files a Schedule 14D-9.

3. Select Metrics and Multiples

As in Comps analysis investors must select relevant financial multiples and ratios to perform their analysis. Measures including size, profitability, growth and returns must be taken into consideration.However, precedent transactions differ to comps as investors usually rely on LTM revenue and EBITDA instead of making future estimates since forward projections for acquired companies are often unavailable or inconsistent.

It’s also important to consider the form of consideration—whether the deal was structured as all-cash, all-stock, or a cash-and-stock mix. This affects both valuation and the nature of the premium, especially in volatile markets where stock-based offers fluctuate in value.

Equity Value Multiples

These multiples focus solely on the value attributable to shareholders, excluding the effects of debt or cash on the company’s balance sheet.

- Offer Price per Share / LTM Diluted EPS

- Equity Value / LTM Net Income

Enterprise Value Multiples

These multiples are widely used in valuation because they reflect the total value of a company including both, debt and equity.

- EV/ LTM EBITDA

- EV / LTM EBIT

- EV / LTM Sales

Premiums Paid

Investors must take into account the premiums paid because of synergies. This concept refers to the extra money paid (in dollars) per share from the acquirer related to the unaffected share price expressed as a percentage.

- (Offer Price per Share / Unaffected Share price) – 1

4. Determine the Valuation

Once the necessary information has been gathered, investors assess the valuation range for the target company. Although valuation standards can vary significantly across different industries the most relevant multiples when performing this analysis are Enterprise Value to EBITDA (EV/EBITDA) and Equity Value to Net Income.

Investors calculate mean and median along with percentiles such as the 75th or the 25th percentile to assess the valuation. Closest comparables are given more weight in this analysis. If an investor calculates an average EV/EBITDA multiple of 6.0x but the multiples for the closest comparables fall within the interval 5.0x to 5.5x, it may be more reasonable to adjust the valuation range to something like 5.0x to 6.0x.

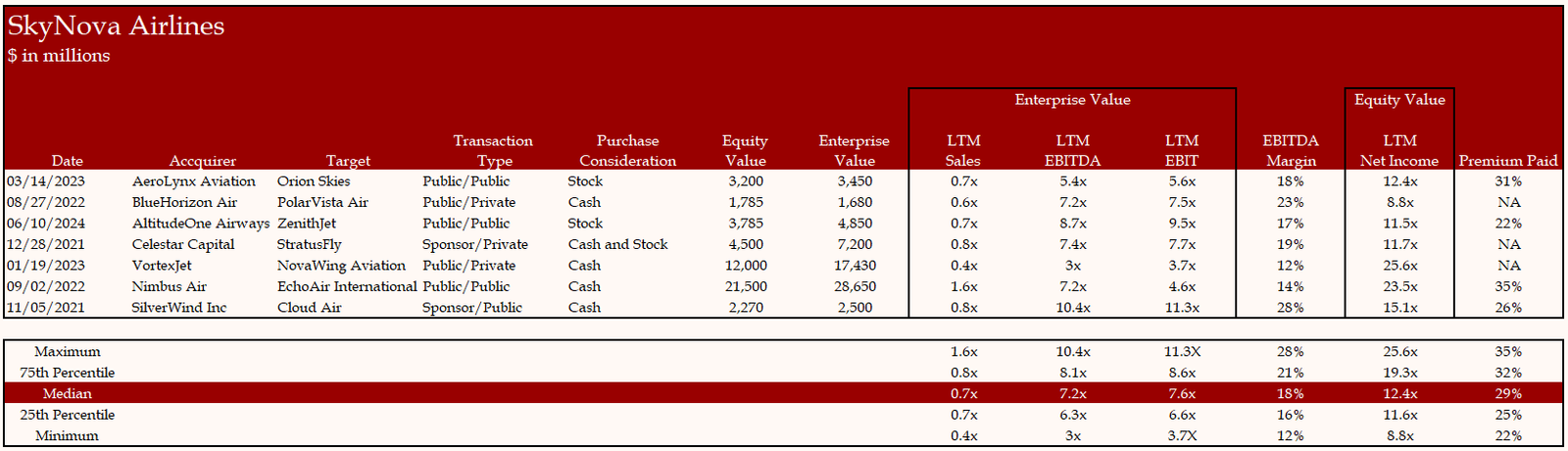

Below investors will find an example of a Precedent Transactions Analysis using SkyNova Airlines as the target. For detailed information about this last step investors can check the Last Step of the Comparable Companies Analysis.